Forum Replies Created

So you had $150k more in your bank account the day you bought? The same week then? Same month?

The day after you bought, your property’s new value was precisely the amount you paid for it.

But given time and other sales (hopefully higher valued comparable sales) then your property might have been valued $150k higher … later. But not when you bought. There’s no discount flip strategy.

If you genuinely did buy way under value AND if nobody else did (so prices didn’t plummet), then given time for the market to consider your purchase as a one off anomaly, then you’ve made your $150k. But not when you bought.

If you did make your money when you bought, then you could repeat it every weekend or at least every month.

Imagine making $150k every week. Even every month is pretty good. I wouldn’t bother holding for a measley bit of rent, repeat the magic every week.

If you really do make money when you buy, then repeat that buying process as frequently as possible. The fact you can’t repeat it every week, not even every month, proves that you don’t make money when you buy.

Jeremy Sheppard

https://selectresidentialproperty.com.au/My point is that even if you invest wisely, it takes time for that wisdom to play out and recover the expense of buying. At the instant of buying, you have already lost money whether it was an astute decision or not.

Jeremy Sheppard

https://selectresidentialproperty.com.au/Well, buying under-valued props is a whole ‘nother topic.

This topic is about buying under the median. You can buy under the median and still pay too much. Conversely, you can buy over the median and nab a bargain.

But a nice case study. Assuming you pay an agent $7k to sell it and your base profit was $75k, then prior to tax you’ve made $68k.

Assuming you’ve held it for more than 12 mths prior to selling, you get the 50% CGT discount, so the tax at your marginal rate is based on $34k. Assuming 40c in the dollar marginal tax rate, you’d pay $13,600 in tax leaving you with $54,400. Nice.

Ah, but then there’s about $2,000 in holding costs, depending on how long the property is vacant.

Calculating a return on your investment: 20% deposit plus 5% stamp duty legals and inspections = 25% of $220k = $55k. Plus reno costs of $45k = $100k investment. Which means you’ve got a 52.4% return on investment (52400 / 100000). That’s better than simply holding for growth – assuming you got growth at the long-term national growth rate of 6%.

Let’s say you got 10% growth on a 25% investment ($55k deposit and 5% other entry costs) and the property was neutrally geared…

10% of 25% is 40% ROI for sitting on your hands and allowing growth to do its thing. A fair shy short of 52%. So the effort to renovate was worth it.

Jeremy Sheppard

https://selectresidentialproperty.com.au/There’s no such thing as the discount-flip like there is for the reno-flip…

You can’t buy an under-valued property and then sell it for market value next month. If that’s the strategy, you won’t make much money. So, what is a useful strategy then?

If you buy under market value AND get capital growth, that would work – but over time obviously. You want that time to be as quick as possible. You want immediate capital growth.

The problem is, the best markets for capital growth are the worst markets for buying under valued property and vice-versa. Hence why attempting to buy under value may not be the smartest strategy.

Jeremy Sheppard

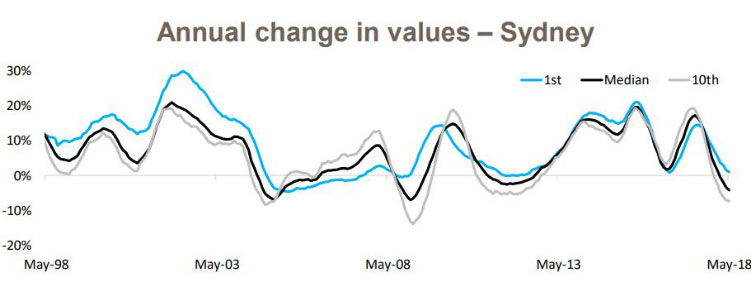

https://selectresidentialproperty.com.au/Yes, good point about the relative risk associated with price point. Core Logic have published a fair bit of data along those lines. Like this chart…

Although it’s deciles within a city, there’s no reason to believe the same concept doesn’t apply to properties within a suburb.

But I dunno about rent. If the market goes pear-shaped, landlords lower their rents across the board to whatever the market demands. If expensive property asking rents are lowered to avoid extended vacancy, they might come down towards the same rents as cheaper properties. But then landlords of cheaper properties would also have to lower their expectations. It trickles down. So, cheap and expensive come down together to meet the lower demand.

Anyway, there’s certainly no “dragging up” effect by aiming to buy under the median for the suburb. But valid point about the risk, especially for the short-term.

Jeremy Sheppard

https://selectresidentialproperty.com.au/The whole point is the plan an investor has for the property. If an investor’s focus is on making money when they buy, they may not have a plan in place for the property after they buy it. They may simply be trying to buy a bargain. They think they’ve made money when they bought. But they haven’t.

By instead focusing on what happens after the property is bought, you’re more likely to realise a profit. E.g. reno, subdiv, dev, cap growth, yield etc. All of those strategies require a plan prior to buying and an implementation of that plan after buying.

In the case of cash-flow, the investor will focus on the income vs expenses and vacancy rate and landlords they’re competing with for tenants.

In the case of capital growth, the attention is given to supply and demand.

In the case of a reno, the investor estimates costs and new value.

In the case of … etc.

The focus is not on buying cheaply. The focus is not on making money when you buy. The focus in all these cases is on making money after you buy.

It’s that focus I’m talking about. Buying cheaply isn’t a feasible strategy. There’s no such strategy as the discount flip because we lose money when we buy.

Jeremy Sheppard

https://selectresidentialproperty.com.au/Ok, I didn’t see that case on your website. Admittedly I didn’t look far sorry.

But technically you’re not buying, you don’t complete the purchase, you sign the contract but don’t settle.

Real estate agents make money by being involved in the transaction, but they don’t buy. Solicitors too.

Your case is a different role, “securing” the property and onselling the right to buy, much like a ‘call’ option.

But technically you’re not buying the property. If you were to buy the property, you would pay stamp duty. That would put you behind.

I guess if an investor bought off the plan and had a long delay to settlement and during that time they’re was some capital growth, then at the time of settlement (buy) they may have made some equity. But then you could argue they lost money at the time of signing the contract – legal fees, deposit bond, etc.

Jeremy Sheppard

https://selectresidentialproperty.com.au/I checked out your website HomeBuyerLouisiana. As I thought, you don’t make money when you buy. The very 1st case study on your website says you put effort and money in.

As I mentioned in the full article, investors make money when they hold OR ADD VALUE. You’re making money by adding value – not when you buy. The buying part may represent a FUTURE opportunity, but you don’t actually make money WHEN you buy. It sounds pedantic, but there’s an important point behind it…

Investors sometimes think they’re locking in “instant equity” at the time they buy, if they buy under market value. But there’s no such strategy as the “discount flip” like there is for a “reno flip”.

It sounds like you’re making money from adding value. Nothing wrong with that. But the point is, there’s no such thing as instant equity simply from buying cheap. In your case, effort has to go into “doing up” the property before a gain can be realised. In my case, I’m allowing time to pass to gain equity.

You may have bought a great “opportunity” to apply a strategy and make a gain. But at the time of buying the property, you’re behind. Something has to happen “AFTER” the purchase to make the gain. In your case, it’s a reno. In my case it’s sitting on my hands and collecting equity. But none of it happens at the time of purchase. On the contrary, we lose money at the time of purchase.

The focus for the investor should be on what happens after they purchase, what’s their plan? Is it to renovate, is it to subdivide, develop or hold for cash-flow or equity or a combination? The buying is not where the focus should be, but on what happens after buying. That’s where the money is made. But when you buy, you lose money.

-

This reply was modified 4 years, 10 months ago by Jeremy Sheppard.

Jeremy Sheppard

https://selectresidentialproperty.com.au/I buy for cash and then did up the house

Sounds like you made money by adding value – “…did up the house…”

Here in Australia, you lose money when you buy. Stamp duty is the big one.

You make money when you add value or hold on and receive rental income and capital growth. But when you buy, you lose money..

The full article explains it best…

https://selectresidentialproperty.com.au/busting/you-dont-make-money-when-you-buy/

Jeremy Sheppard

https://selectresidentialproperty.com.au/Thanks for the kind words Steve. I’d love to chat. I’m Sydney based but in Melbourne till the 19th.

I’ll send you a private message.

Jeremy Sheppard

https://selectresidentialproperty.com.au/Go on.

Jeremy Sheppard

https://selectresidentialproperty.com.au/Hi mnapier,

I get a lot of strong opposition on this topic. Mostly from those who derive revenue from selling new. No apology necessary.

The statement about it being mathematically impossible to outperform is on the assumption that all other things are equal. This wasn’t clear early on in the article. So, I take that criticism on the chin.

The full article goes on to compare 2 properties that are identical in every way except one is new and the other is old. In this case it is impossible for the new to beat the old – mathematically.

Yes, eventually the old property will have to be knocked down and rebuilt. The article covers this case. One plus of this scenario is that the profit is the owner’s not the developers. And yes, as soon as the new property is built, the rate of growth as a proportion of the property’s new value will decrease. And it’s because of depreciation. Buildings depreciate and land appreciates. If more of an investor’s money goes into the depreciable part of the asset (e.g. by capital injection), the performance overall is reduced until the depreciation of that capital injection washes out.

So, although it sounds bizarre, the same property will suddenly start to under-perform in capital growth immediately following a knock-down-rebuild. And the reason is depreciation of the capital injection.

There is nothing beneficial about depreciation for those pursuing appreciation. Many make the mistake of assuming depreciation is simply a tax write-off. But depreciation is a real thing. An investor’s dwelling ages and therefore loses value.

Yes, you should claim depreciation, but you shouldn’t go hunting for properties with higher rates of it. Since every bit of depreciation opposes appreciation.

If you can claim $10k in depreciation for a financial year and you’re paying 40c in the dollar tax, you’ll pay $4k less tax. But this is not a benefit. The investor is not “better off” by $4k. They are actually worse off by $6k compared to not having any depreciation at all – i.e. their dwelling barely aged.

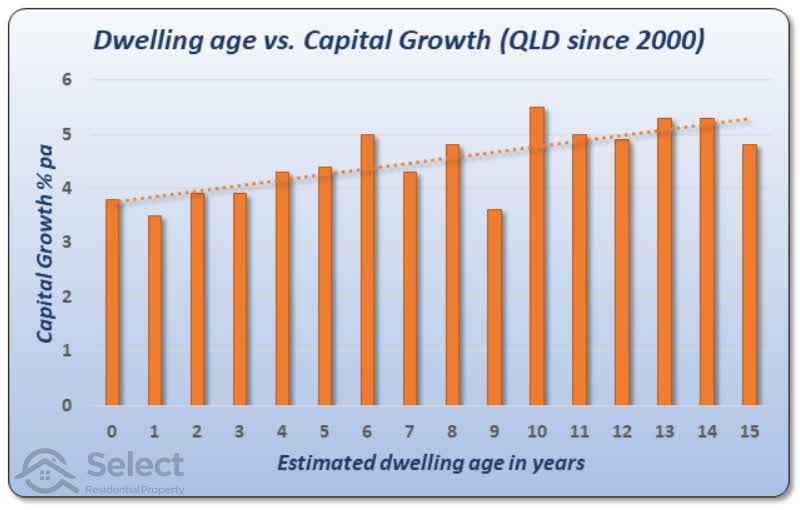

Older properties do not depreciate as significantly as newer ones and therefore have better appreciation. The chart clearly shows the relationship between age and growth.

The law of supply & demand is about 400 years old and is a fundamental of price change. To see maximum growth in the price of anything, there needs to be minimum supply and maximum demand. I suspect you’re not arguing against that. But whether new property represents supply. I do, but even if it isn’t called “supply” whatever it is called, there is a relationship between lower growth and whatever it’s called as the historical data indicates.

Something that would lend more credit to your arguments would be some supporting data. It took me months to acquire the data, analyse it and write up the report…

https://selectresidentialproperty.com.au/busting/new-properties-under-perform/

The purpose of the series was to “show up” opinions with a stack of evidence. Opinions are plentiful and cheap. Perhaps you’re examining a different data set to me. What are your sources?

Jeremy Sheppard

https://selectresidentialproperty.com.au/Hi Jaxon, we could have two differently priced properties and compare their growth rates as opposed to the dollar difference.

The point is that the rate of growth is dependent on the appreciation rate of the land and the depreciation rate of the dwelling.

Here’s a cool chart that only takes a few minutes to get the gist, but took me literally months to acquire the data, import into the database and perform calculations…

Dwelling Age vs Capital Growth

New property has lower growth rates than old property in general. And it’s due to the typically lower land-to-asset ratio newer properties have.

Jeremy Sheppard

https://selectresidentialproperty.com.au/-

This reply was modified 4 years, 10 months ago by